EPR Revolution: How Turning Packaging Compliance into Competitiveness Gives Brands an Edge

What is Extended Producer Responsibility (EPR) in packaging?

Extended Producer Responsibility (EPR) is a regulatory policy that makes producers, brands, importers, and manufacturers, financially and operationally responsible for the end-of-life management of the packaging they place on the market. Under EPR, producers pay fees into a system that funds collection, sorting, and recycling infrastructure. Fee levels are typically modulated by material type and recyclability, meaning packaging design decisions directly determine compliance cost.

EPR Is No Longer a Horizon Risk, It Is a 2026 Operational Reality

Seven US states have now passed packaging EPR legislation. What began as a sustainability discussion has moved into finance, procurement, and supply chain. Brands selling into California, Oregon, Colorado, or Maine face producer registration and fee payment obligations beginning as early as 2026. By 2031, Maryland, Minnesota, and Washington will follow.

For multi-state producers managing diverse packaging portfolios, the combination of different state definitions, fee models, and reporting timelines creates a compliance complexity that cannot be managed reactively. The time to build internal readiness is now, not when the first invoice arrives.

Packfora's position on EPR is direct: this is not a sustainability project to be delegated to the ESG team. It is a strategic inflection point that touches financial modelling, packaging design, procurement strategy, and brand accountability simultaneously.

Why Acting Now Matters: The 2026–2031 Timeline

The regulatory rollout is staggered, but the preparation window is shared. Brands that begin compliance modelling only when their first active state deadline arrives will face compressed timelines, limited design options, and potentially sub-optimal material decisions made under time pressure rather than commercial logic.

| State | Deadline | Key Requirement | Status |

|---|---|---|---|

| California | By 2026 | Register + pay EPR fees; SB 343 recyclability labelling | Law passed |

| Oregon | By 2027 | Producer registration and fee payment | Law passed |

| Colorado | By 2027 | Producer registration and fee payment | Law passed |

| Maine | By 2027 | Producer registration and fee payment | Law passed |

| Maryland | By 2031 | Producer registration, reporting and fees | Law passed |

| Minnesota | By 2031 | Producer registration, reporting and fees | Law passed |

| Washington | By 2031 | Producer registration, reporting and fees | Law passed |

Beyond the seven states with passed legislation, ten additional states introduced packaging EPR bills in 2025 alone: Connecticut, Hawaii, Illinois, Massachusetts, Nebraska, New Jersey, New York, North Carolina, Rhode Island, and Tennessee. The directional signal is unambiguous, national coverage is the trajectory, not the exception.

Packfora Recommendation

Start with a Scope and Exposure Diagnostic. Map where your products are sold, identify which SKUs fall under EPR, and quantify cost exposure under multiple material scenarios.

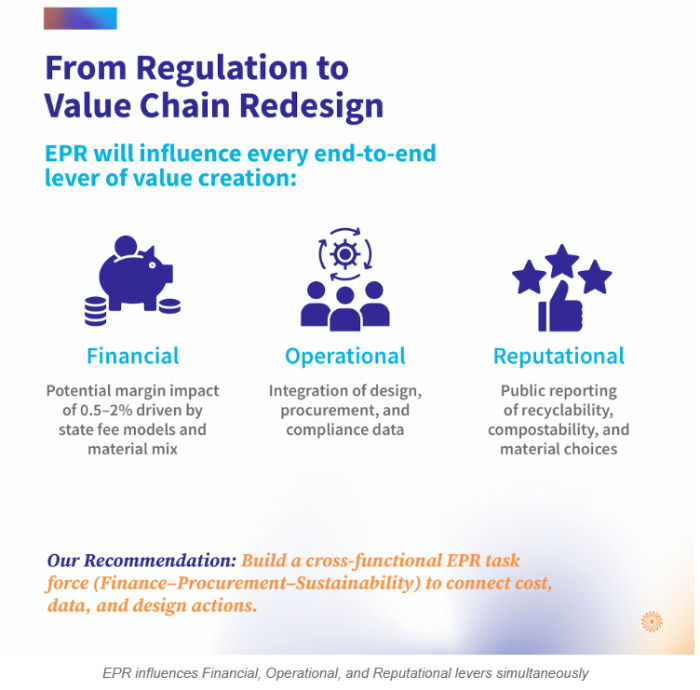

From Regulation to Value Chain Redesign

EPR does not sit in one function. Its impact runs across three distinct dimensions of value chain performance:

| Impact Area | What EPR Changes | Action Required |

|---|---|---|

| Financial | 0.5–2% potential margin impact from state fees and material mix | Model fee exposure by SKU and material type across all active states |

| Operational | Design, procurement, and compliance data must be integrated, not siloed | Build cross-functional EPR task force: Finance + Procurement + Sustainability |

| Reputational | Public reporting of recyclability, compostability, and material choices mandatory | Ensure packaging claims are accurate and defensible, SB 343 labelling risk is real |

The 0.5–2% margin impact figure is not a worst-case scenario, it is the realistic range for brands with significant packaging volumes operating across multiple EPR states with mixed material portfolios. For a brand with $500M in revenue and packaging-intensive categories, that range represents $2.5–10M in annual fee exposure.

The brands managing this well are not doing so by accepting the fee as a cost of business. They are using EPR as a forcing function to redesign packaging towards lower-fee materials, improve recyclability performance, and reduce overall packaging complexity, outcomes that deliver commercial benefit well beyond compliance.

Packfora Recommendation

Build a cross-functional EPR task force (Finance–Procurement–Sustainability) to connect cost, data, and design actions. EPR managed in silos produces compliance, EPR managed cross-functionally produces competitive advantage.

Seven States. Seven Systems. One Packaging Portfolio.

The structural challenge for multi-state producers is definitional inconsistency. Each state defines three critical concepts differently:

- who is responsible (brand owner, importer, first-to-market) varies by state Producer

- what qualifies as recyclable or compostable is not standardised across state frameworks Recyclability

- how fees are adjusted for material type, recycled content, and recyclability performance differs significantly Fee Modulation

A packaging specification that performs well under California's framework may carry higher fees under Oregon's model. A material that qualifies as recyclable in Colorado may not meet Maine's definition. Managing this mosaic with a single static compliance report is not viable at scale.

What is required is a unified data architecture, a single source of truth that aligns SKU-level packaging data, material composition, state-specific sales volumes, and regulatory definitions, enabling accurate fee simulation and reporting across the entire portfolio simultaneously.

Packfora Recommendation

Create a unified EPR data layer that aligns SKU, material, and sales data across states, enabling centralised reporting and simulation. This infrastructure is the prerequisite for everything else.

Packfora's structural packaging consultancy supports brands in designing packaging that meets EPR recyclability requirements without compromising performance, reducing fee exposure through design intelligence rather than cost escalation.

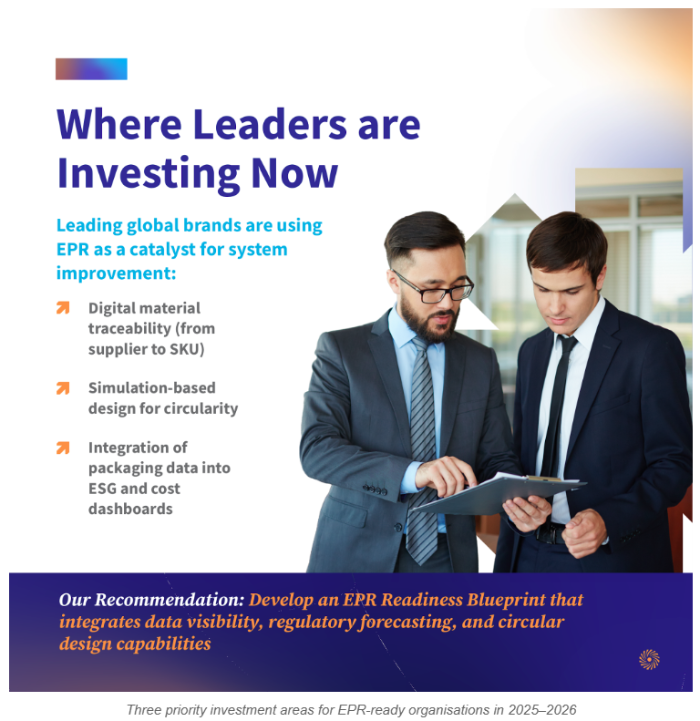

Where Leading Brands Are Investing Now

The brands using EPR as a catalyst rather than a burden are making three specific capability investments:

- Digital material traceability from supplier to SKU, knowing exactly what is in every pack, at material and component level, is the foundation of accurate EPR reporting

- Simulation-based design for circularity, using tools like FEA and material modelling to evaluate packaging design changes against both performance and EPR fee impact before committing to specification changes

- Integration of packaging data into ESG and cost dashboards, making EPR exposure visible at board level, not buried in compliance reports

These are not aspirational capabilities, they are the minimum infrastructure for managing EPR at the scale and complexity that multi-state producers face. Brands that build them now will have a structural advantage over competitors who treat EPR as a reporting exercise.

Packfora Recommendation

Develop an EPR Readiness Blueprint that integrates data visibility, regulatory forecasting, and circular design capabilities. This blueprint becomes the operating model for EPR compliance across all states and timelines.

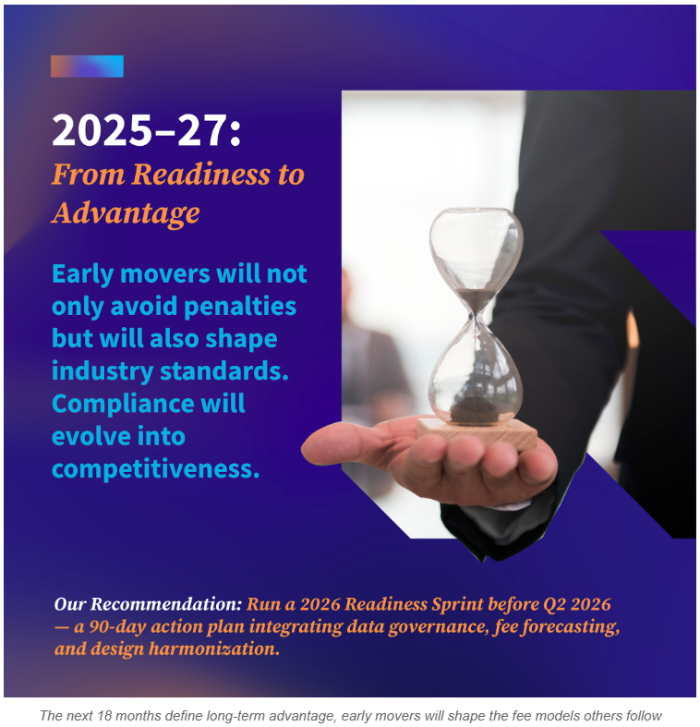

2025–27: From Readiness to Competitive Advantage

The window between now and 2027 is not simply a compliance preparation period. It is the period in which the standards get set, who defines what recyclability means in practice, which material strategies become the industry norm, and which brands earn the reputational benefit of leading on packaging responsibility.

Early movers in EPR do not just avoid penalties. They participate in shaping the Producer Responsibility Organisations (PROs) and fee modulation frameworks that will govern their competitors. That is a structural commercial advantage that compounds over time.

Packfora Recommendation

Run a 2026 Readiness Sprint before Q2 2026, a 90-day action plan integrating data governance, fee forecasting, and design harmonisation across your packaging portfolio.

The Packfora Position: EPR as a Design and Strategy Brief

The brands that will win in the EPR era are not the ones with the best compliance teams. They are the ones that recognise EPR as a brief for packaging redesign, material strategy, and supply chain data investment, and act on that recognition before the fee deadlines force their hand.

The next 18 months will define long-term advantage. Early movers will shape the fee models and circularity standards that others will follow. EPR is not a cost line. It is the next competitive differentiator in packaging.

Explore Packfora's sustainability consulting to understand how EPR strategy integrates with your broader packaging and material roadmap.

For packaging teams ready to model their EPR exposure and build a 2026 readiness roadmap, Packfora's Design to Value service connects compliance requirements directly to packaging design and procurement decisions.

Frequently Asked Questions

Which US states currently have packaging EPR laws?

Seven US states have passed packaging EPR legislation: California, Colorado, Maine, Maryland, Minnesota, Oregon, and Washington. California, Oregon, Colorado, and Maine have defined timelines requiring producer registration and fee payments by 2027. Maryland, Minnesota, and Washington follow by 2031. An additional 10 states introduced EPR packaging legislation in 2025, signalling broad national expansion

How are EPR fees calculated for packaging?

EPR fee calculations vary by state, but are generally based on the weight and material type of packaging placed on the market within that state, modulated by recyclability performance. Materials with higher recyclability rates typically attract lower fees; non-recyclable or difficult-to-recycle materials attract higher fees. Some state frameworks include additional modulation for recycled content percentage. Because each state defines its own fee model, brands operating across multiple states must calculate exposure separately per jurisdiction.

What is the financial impact of EPR on packaging brands?

Packfora estimates a potential margin impact of 0.5–2% for brands with significant packaging volumes operating across multiple EPR states. The exact figure depends on material mix, sales volume by state, and packaging recyclability performance. For brands with large, packaging-intensive portfolios, early investment in EPR readiness, including packaging redesign towards lower-fee materials, can significantly reduce fee exposure compared to a reactive compliance posture.

What is the difference between EPR and a plastic packaging tax?

A plastic packaging tax is a direct levy on packaging that does not meet a defined recycled content threshold, collected by the government (e.g. the UK's £217.85/tonne tax on packaging with less than 30% recycled content). EPR is a broader system that makes producers responsible for funding end-of-life packaging management, collection, sorting, and recycling, typically administered through a Producer Responsibility Organisation (PRO) rather than direct government collection. Both create financial incentives to improve packaging recyclability and recycled content, but through different mechanisms.